Firstly, what exactly is ‘The Register of Overseas Entities’?

The Register of Overseas Entities in short is, a public register of the verified details of the ‘ultimate beneficial owners’ (UBOs) of overseas entities that own UK property.

The overriding purpose of the register is to tackle money laundering and economic crime in the UK property market through increased transparency of ownership, and control, by having a public record searchable on the Companies House registry.

Any overseas entity wanting to buy, sell or transfer property or land in the UK must register with Companies House and provide details of the registrable beneficial owners. An overseas entity must also submit an annual ‘Update Statement’ on Companies House, 12 months from the date it was initially registered.

Qualifying Estate means a freehold property or a leasehold interest granted for a term of seven years or more in the UK.

The land registration element of the Act came into force on 5 September 2022 and placed restrictions over titles at Land Registry until the overseas entity obtained an Overseas Entity ID from Companies House.

What is defined as an ‘overseas entity’ and who are the ‘registrable owners’?

OVERSEAS ENTITIES – defined as “a legal entity, such as a company or other organisation, that has legal personality and is governed by the law of a country or territory outside the UK”. Includes Jersey incorporated companies that are UK tax resident (these may not be registered with Companies House, but will now be subject to register if they hold any UK property or land).

REGISTRABLE OWNERS – can be an individual, legal entity or government/public body which is determined based on the nature of control if one or more of the following four conditions are met:

i. They hold, directly or indirectly, more than 25% of shares in the entity

ii. They hold, directly or indirectly, more than 25% of the voting rights in the entity

iii. They hold the right, directly or indirectly, to appoint or remove a majority of the board of directors of the entity

iv. They have they right to exercise, or actually exercise, significant influence or control over the entity

If there are no beneficial owners, or not all beneficial owners have been identified, then the details of the managing officers of the overseas entity will need to be provided. This could be a director, manager, or company secretary of the overseas entity.

What information is required?

The Overseas Entity; Registrable Beneficial Owners; and Legal Entities will each be required to submit information as part of the registration process.

REGISTRABLE BENEFICIAL OWNERS can be an individual, legal entity or government/public body. Individuals must provide name, date of birth, nationality, correspondence address and home address, date they became a beneficial owner and nature of control.

LEGAL ENTITIES will need to provide their name, registered office address, correspondence address, legal form and governing law, public register it appears on and registration number (if applicable), date they became a beneficial owner and nature of control. For example, this could be a corporate trustee of an overlying trust.

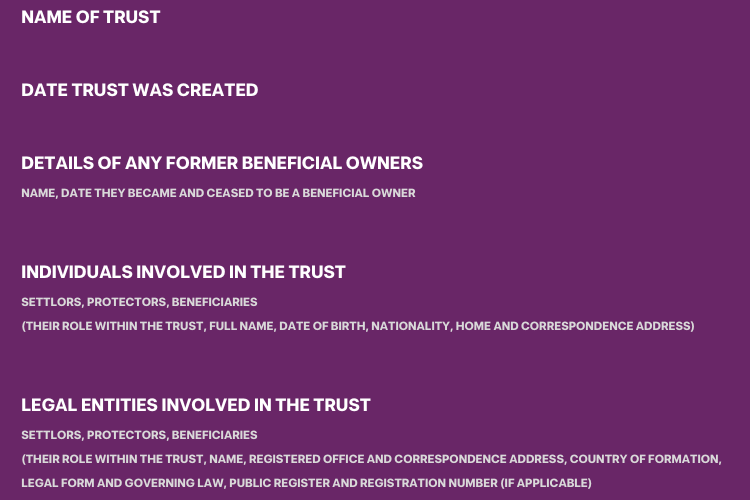

TRUSTS

Where a trustee of a trust has been identified as a ‘registrable beneficial owner’ very specific information is required, including:

What is a ‘Verification Check’?

A UK-regulated agent must complete the ‘verification check’ on all beneficial owners of an overseas entity before it is registered. This is also the case when submitting the Update Statement if there have been any changes, if one of the registrable beneficial owners has changed home address for example.

The UK-regulated agent must be based in the UK and supervised under the Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017. They can be an individual or corporate entity. Once they have completed their verification checks, they will provide us with an agent assurance code and overseas entity verification statement to confirm this has been done, which is then submitted to Companies House.

What is the ‘Update Statement’?

Companies House launched their online service for Update Statements in 2023. This is a statement to confirm to Companies House that all the information held on the register is correct and up to date.

A UK-regulated agent must complete the ‘Update Statement’ if there have been changes, for example, if one of the registrable beneficial owners has changed home address.

N.B. A statement must be filed even if nothing has changed.

If I don’t file, what are the implications?

Overseas entities not registered on Companies House will face restrictions on selling, transferring, leasing or raising charges against their property/land and they also cannot purchase any new UK property without an Overseas Entity ID.

Furthermore, it is a criminal offence to not file an Update Statement.

Companies House has advised that they will soon be issuing financial penalties to those who have not registered.

The Overseas Entity no longer holds UK property or land, what do we need to know?

As of 20th February 2024, the process for the removal of an overseas entity remains under development, however, if an overseas entity has fully disposed of all UK property and land, you should note that:

i. Companies House must be ADVISED of the disposal and provided with the Overseas Entity ID.

ii. An ‘Update Statement’ will not need to be submitted.

As part of the removal process, the Registrar is also required to check with the three UK Land Registries that the overseas entity has disposed of all property within the UK before processing such an application. The Land Registry is currently working to develop a system to allow these checks to take place in an efficient manner.

Next steps?

If you’re unsure of your position in relation to The Register of Overseas Entities our team are available to dscuss the above in greater detail with you.

Please contact our Tax Manager, Amy Brown.

FURTHER GUIDANCE FROM THE DEPARTMENT OF BUSINESS AND TRADE, IS AVAILABLE HERE