Furthermore, professional trustees may be cautious to avoid an over concentration of trust assets into a particular class of asset; a Private Trust Company is better able to allow investment into a single class of asset, for example shares in the family business.

Like any other company, a Private Trust Company is run by its board of directors while the administration of the Private Trust Company and underling family trusts, is carried out by a regulated service provider.

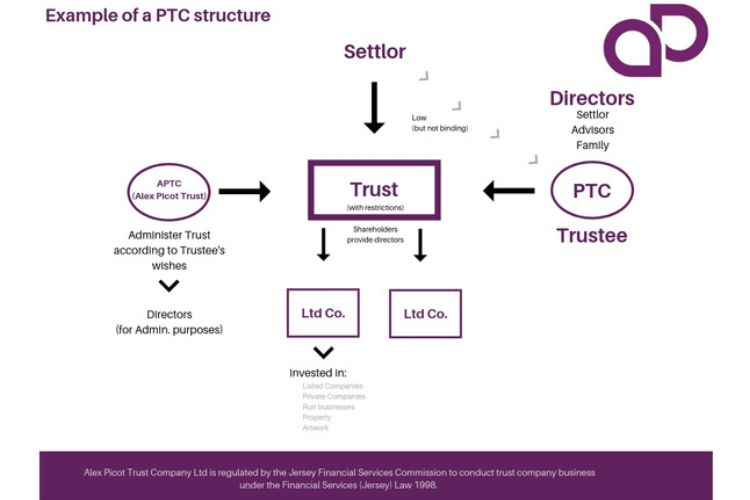

The board of directors typically includes family members who can ensure that the wishes of the founder of the trust are given proper consideration and enable them to become familiar with, and participate in, decision affecting the family assets.

It is not a requirement that only family members are appointed to the board of a PTC and trusted advisors can also fill these roles.

Trust structure using a Private Trust Company

When it comes to a Private Trust Company, the role of trustee is performed by a separate company, owned by a stand-alone purpose trust, foundation or the individual Settlor; which would have as its potential directors, the Settlor, members of the Settlor’s family and /or their advisers.

These persons will be more aware of the Settlor’s objectives and family issues than external trustees. The only stipulation from a Jersey point of view is that the Trust is administered by a Jersey regulated and licensed business.

As in a standard Trust structure, the Settlor is free to issue a Letter of Wishes. He can also set out the conditions for the control of the Private Trust Company, thus ensuring that the Private Trust Company, as Trustee, works to pre-established objectives.

By being directly able to direct underlying investments, which may also involve the same people, the decision making process is shorter than if a protector was involved. The Trustees may also be willing to take a less cautious approach to investing than a professional trustee might.

However, for added restrictions and comfort, a Protector can be included in the structure.

Reporting requirements

Jersey has no ‘public register’ of Trusts or Private Trust Companies.

However, there is soon to be a requirement to advise the Jersey Financial Services Commission (JFSC), on a confidential basis, of the identity of the Settlor of Trusts.

Under the Common Reporting Standard (CRS) and FATCA, there is a duty to report to the Jersey tax office, who then distribute to affiliated countries, distributions made, details of the Settlor and in some cases the value of the trust fund where those concerned are connected to the countries that have signed up to CRS and FATCA. This is not made publicly available.

In Jersey there is a requirement to report to the JFSC the beneficial owners of a Jersey company, and if held by a Trust, the Settlor of that trust.

For Jersey companies there is a public register of company name and details of shareholders, though the latter may be held by our nominees, thus ensuring confidentiality from casual and not so casual observers.

Taxation in relation to a Private Trust Company

At the current time, and we are not aware of any suggested changes, the only time the entities

within the structure would become subject to Jersey tax is if any of the beneficiaries became Jersey

resident, or if investment was made in Jersey property.

Only net rental income would be taxed, there being no capital gains taxes in Jersey.

Where investments are made we would request to receive reports from managers, either by annual accounts or a quoted price or valuation.

Controls over the level or frequency of distributions can be easily put in place, although these are very much something for the Settlor (or Private Trust Company or Protector) to stipulate.

Policies and Controls

In respect of setting up and administering a Private Trust Company, the procedures of Alex Picot Trust Company would be followed, subject to any specific reference in the Trust Deed.

As regulated entities of Alex Picot Trust is obliged to follow the Financial Services Law and consequently the Money Laundering Jersey law.

We have an internal procedure to obtain an indemnity for any distribution over £50,000, however, this could be increased or removed in the case of a Private Trust Company structure.

Other controls that we operate concern the signatures required over distribution of assets.

Every distribution that is made requires the authorisation of two approved signatories.

The only people authorised to take on this role as Directors of Alex Picot Trust Company, alternate Directors and Senior Trust Officers within our organisation.