Valuation

There are four components that make up the value of the UK residential property for Inheritance Tax purposes:

1. UK residential property

2. Loan used to acquire, maintain or enhance a UK residential property

3. Collateral / security used for the loan

4. Nil rate band (currently £325,000)

The property is the probate value for death tax, or the value at the date of the 10-year anniversary for ongoing trust charges. Any proceeds received on the sale of a residential property will remain within the charge to IHT for two years after a disposal. This is important to note if planning is being taken around the 10-year anniversary of the trust it is advisable to dispose of the property in the 8th year rather than the 10th year to avoid being subject to IHT.

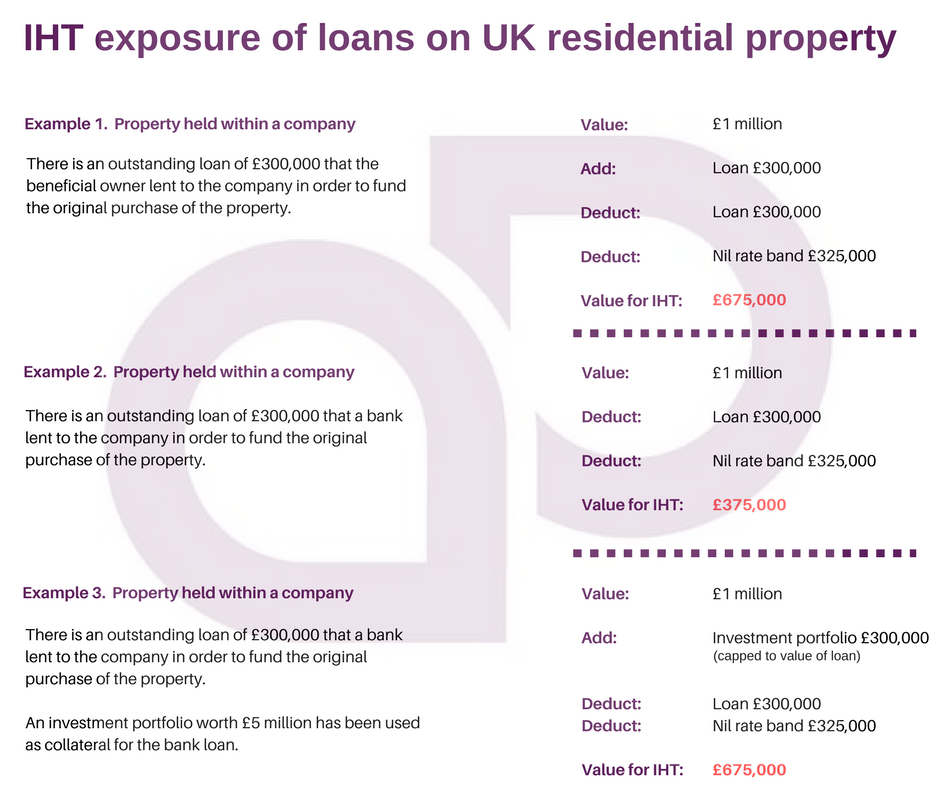

Loans

Loans are still deductible for inheritance tax purposes regardless of whether the lender is a connected party. However, if the loan is non-commercial or made by a connected party, its value will be added to the value of the UK residential property, effectively leaving the individual no better off.

This add back does not apply to loans made to non-close companies (5 or more participators). Any loans from connected parties should be looked at in advance of April 2017.

Collateral

Collateral behind loans adds to the value of the property, even if the loan is commercial and from a third party i.e. a bank. This could significantly increase the value of the property and therefore the tax.

The account that the collateral adds to the value of the loan is capped at the value of the loan – so again, if a bank loan with security, you will be left in a neutral position as the loan will be deducted and the same amount of collateral added back.

Prior to April 2017, loan arrangements with collateral should be reviewed to assess whether the collateral is required.

Examples

For further information please contact our Tax Consultant Hannah Roynon-Jones.