Background

The UK Government has introduced a ‘protected settlement’ regime for non-UK trusts settled by individuals before they become deemed domiciled in the UK.

Under the protected settlement rules, the settlor is protected from the attribution of trust gains (see section 86 of the Taxation of Chargeable Gains Act 1992) and the attribution of trust income (settlor interested trust provisions).

Therefore the ‘protected trust’ rules broadly allow for income and capital gains to roll up within such trusts without UK tax charges – provided that is that the settlor makes no direct or indirect additions to the trust after they have become ‘deemed domiciled’ in the UK.

Protected trusts will continue to have “excluded property” status for IHT purposes.

So, it’s good news for the settlor?

Certainly, for those settlors taxed on the arising basis these rules offer some positivity and have the potential to leave them better off.

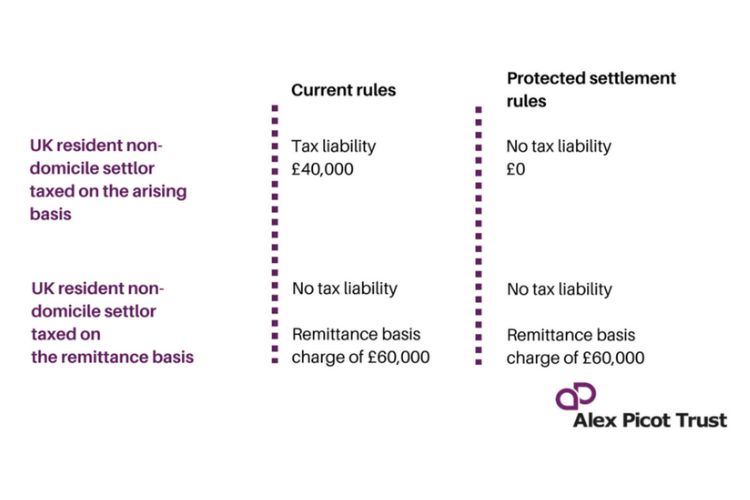

To illustrate this let’s look at a trust that is established by a UK resident non-domiciled individual. Let’s imagine it has an underlying company that holds an investment portfolio which has generated £100,000 income this year; the settlor is a higher rate taxpayer; and has been UK tax resident for 13 years.

Comparing the settlor’s options under the current rules and the new ‘protected settlement’ rule due in April 2017.

Under the protected ‘settlement rule’, a settlor who is a remittance basis taxpayer would have to consider whether it was still worthwhile paying the remittance basis charge as the income and gains of the trust structure would no longer be attributed to them. This would depend on the level of any other offshore income/gains they had.

Beware some conditions

The trust must be established by a UK resident non-domiciled individual (before 6 April 2017).

The settlor cannot be deemed domiciled.

The settlor cannot be a ‘returning UK dom’ i.e. UK resident with a UK domicile of origin.

The settlor is protected from the attribution of trust income and gains as they arise.

The protected settlement also offers inheritance tax protection as it is an excluded property trust.

The protection is lost where property is added to the settlement later when the settlor is UK domiciled i.e. becomes deemed domiciled in the future.

Settlors will be taxed on income in respect of matched distributions made to beneficiaries who are non-UK resident and close family members.