It’s almost two years since Capital Gains Tax was extended to non-residents disposing of UK residential property, yet the filing deadline continues to pose a problem.

Non-resident Capital Gains Tax (NRCGT) applies where there has been a disposal of UK residential property, regardless of how the property is held (this differs to ATED, which only applies to properties held within a company).

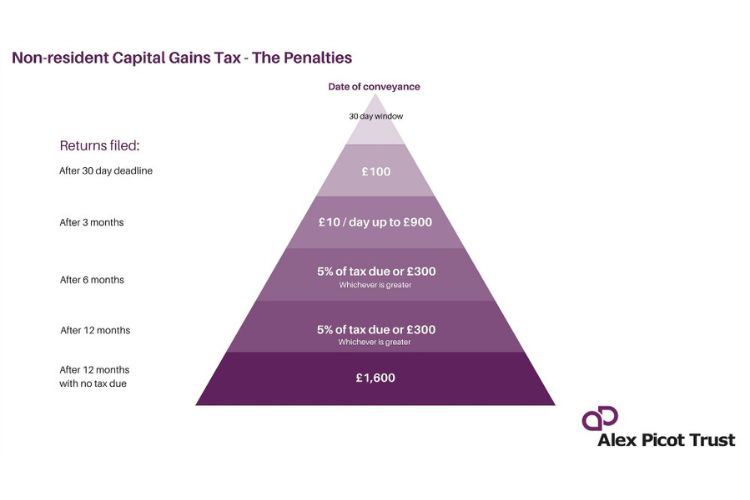

The issues arise around the 30-day deadline. HMRC must be notified of a disposal within 30 days from date of conveyance and any tax due must also be paid within the same period. This quick turnaround is catching people out, especially compared to other tax deadlines which often allow anywhere up to 12 months.

What you need to know

A disposal must be reported within this deadline even if:

- you’ve no tax to pay

- you’ve made a loss

- you’re registered for self-assessment

- you’re registered with HMRC for Corporation Tax

- you send HMRC Annual Tax on Enveloped Dwellings (ATED) or ATED-related Capital Gains Tax returns

The only exception is if you are already registered for UK tax under self-assessment, and the payment can then be deferred until the normal due date of 31 January following the end of the tax year.

Computation

- Disposals will automatically receive an uplift of the base cost of the property to its April 2015 valuation.

- You can elect to dis-apply the rebasing and use straight line apportionment, if this produces a more favourable result.

- Properties being transferred out of structures or gifts of properties count as a disposal for capital gains tax, regardless of whether any money has been received.

- Disposals will benefit from a deduction for indexation.

Administration

- The return must be filed within 30 days of disposal.

- The return can be filed on an estimated basis if final figures are not available.

- The tax due is also payable within 30 days of disposal. This puts even more pressure on filing as you need to obtain a payment reference number from HMRC. Payment references are given once the return is filed.

The late filing penalties applied are the same as they are under Self-Assessment. Even where there is no tax due, if the return is filed late, penalties will apply.

- The late filing penalties applied are the same as they are under Self-Assessment. Even where there is no tax due, if the return is filed late, penalties will apply.

- The late filing penalty is £100 if the return is less than 3 months late.

- For returns filed more than 3 months late, a daily penalty of £10 a day will be charged for 90 days (max £900).

- For returns filed more than 6 months late, an additional penalty of the greater of £300 or 5% of the tax due will apply.

- For return filed more than 12 months late, an additional penalty of the greater of £300 or 5% of the tax due will apply.

- Where the return is filed more than 12 months with no tax due, the late filing penalty will be £1,600. This can cause real issues, for example if the property was transferred out of a company and this company has now been liquidated or has no assets remaining.

N.B. Where the return is filed more than 12 months with no tax due, this can cause real issues. One example is if the property was transferred out of a company and this company has now been liquidated or has no assets remaining.

If you have any questions relating to the issues discussed in this blog please get in touch with our Tax Consultant, Hannah Roynon-Jones

For further guidance click here: https://www.gov.uk/guidance/capital-gains-tax-for-non-residents-uk-residential-property