This facility is a surprising but welcome opportunity for any UK resident individuals who have ever claimed the remittance basis of taxation. The facility means that these individuals can bring, foreign income and gains (FIG) earned prior to 6 April 2025, into the UK at a significantly reduced tax rate.

Key features of TRF

- Available to individuals who have claimed the remittance basis of taxation in any tax year up to and including 2024/25

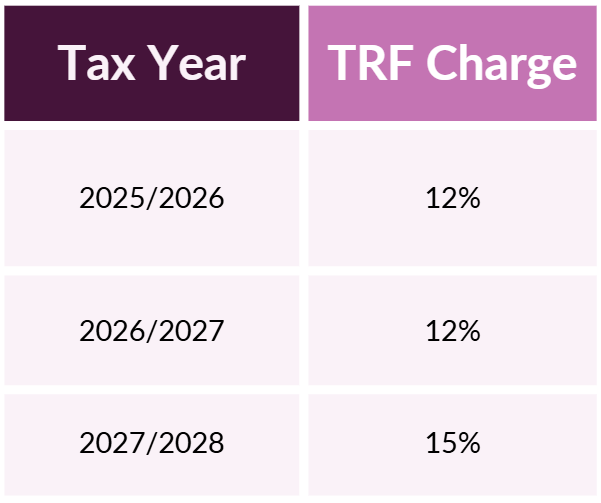

- The TRF will only be available for a limited period of three tax years: 2025/26, 2026/27 and 2027/28.

- It will allow individuals to remit pre-6 April 2025 FIG at a flat rate of either 12% or 15% depending on the year it is received.

- The TRF will not be available for distributions/remittances made out of income or gains that crystallised or were earned after 6 April 2025.

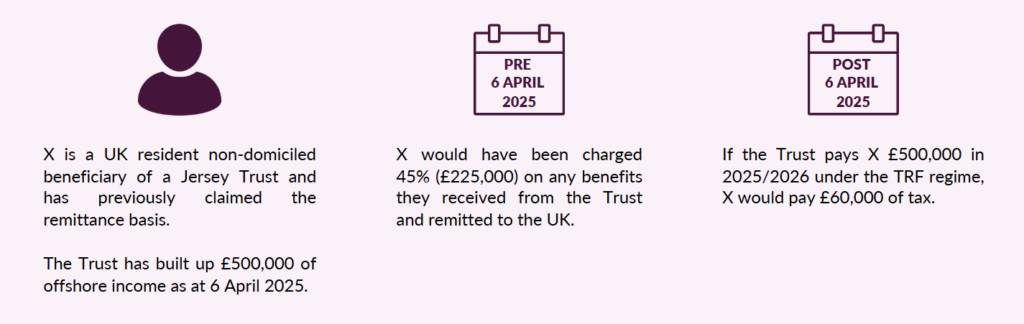

Example

Trustee Considerations

Trustees should be reviewing their structures to make the most of the TRF and identify the most tax efficient time to make distributions.

- Where is the Beneficiary Resident?

- If they are UK resident, are they classified as long-term resident?

- Have they previously claimed the remittance basis?

- If they have not claimed the remittance basis, should they do so on their 2024/25 tax return – last opportunity to claim.

- Are the trustees able to accelerate the realisation/earning/crystallisation of any additional FIG prior to 6 April 2025?

- Consider any distributions or events that were forecast in the medium term that could be accelerated and actioned in the three years of the TRF between 2025/26 and 2027/28.

In conclusion, the TRF presents a significant tax advantage for beneficiaries who are, or were at some point, non-UK domiciled. This three-year window offers beneficiaries a strategic opportunity to bring overseas wealth into the UK in a tax-efficient manner and trustees should be making beneficiaries aware of this limited-time opportunity.

As reminder Alex Picot Trust does not offer advisory services on matters of U.K. taxation.