Who is affected?

Any trust, anywhere in the world, that has a UK tax liability.

All UK taxes are included:

– UK income tax

– Capital Gains Tax

– Inheritance Tax

– Stamp duty land tax or stamp duty reserve tax

Trustees are assumed to be aware of events that may give rise to a UK tax exposure for the trust.

A trust is required to register regardless of the size of its tax liability.

There is uncertainty as to whether this includes a situation where the trustees have an obligation to file a UK tax return but there is no tax liability e.g. makes a loss.

When does the trust need to register?

The trust needs to register on 31 January in the year following the tax year in which the trust had a UK tax liability.

The first deadline for registration is 31 January 2018.

Annual reviews

For those trusts that have not had a UK tax liability in the past or that have previously registered, an annual review is required to check whether they are required to register.

N.B. it is possible to obtain closure letters from HMRC for any trusts which may no longer have a liability to UK tax.

Let’s look at some example scenarios

(All the trusts in the examples are assumed to have Jersey resident trustees and use today’s tax rates and thresholds.)

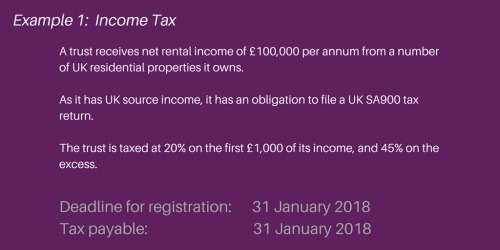

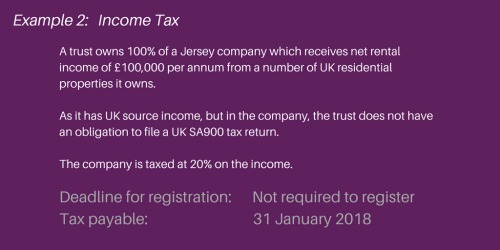

INCOME TAX

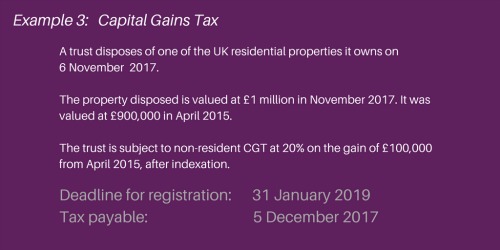

CAPITAL GAINS TAX

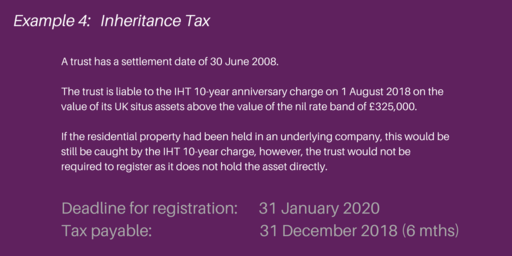

INHERITANCE TAX

INHERITANCE TAX

What needs to be reported?

Once it has been determined that the trust has a requirement to register, the following information must be reported in respect of the trust:

- Name of the trust

- Date of settlement

- Address and tax residence of the trust

- Statement of account of the trust assets

- Names of legal, financial and tax advisors to the trust

In terms of the individuals associated with the trust, this is defined as all ‘beneficial owners’. This is as far reaching as identifying and reporting on ‘potential beneficiaries’ i.e. beneficiaries specifically named in a document such as a letter of wishes that may only be listed in the trust deed as a class of beneficiary. HMRC will rely on the letter of wishes as well as the trust deed as evidence.

The following must be reported on beneficial owners:

- Full name

- National insurance number or UTR

- Residential address (if they do not have a number i.e. minor)

- Date of birth

- Individual’s role in relation to the trust

- Passport number – if they are not UK resident, passport details including the number, country of issue and expiry date must be provided

The UK Trusts Register can be found here.

If you would like to discuss any of the implications of the Trusts Registration Service please contact Hannah Roynon-Jones at Alex Picot Trust.